")

SME Asaan Finance (SAAF) Scheme – The Ultimate Guide for Small Business Owners in Pakistan

Introduction: A Lifeline for Pakistan’s Small Businesses

In a country where small and medium enterprises (SMEs) make up nearly 40% of GDP and employ 80% of the non-agricultural workforce, access to finance remains one of the biggest hurdles. Traditional bank loans often demand heavy collateral, lengthy paperwork, and strict eligibility—putting them out of reach for many deserving entrepreneurs.

Recognizing this challenge, the State Bank of Pakistan (SBP) launched the SME Asaan Finance (SAAF) Scheme, a revolutionary initiative designed to democratize business financing. Unlike conventional loans, SAAF offers collateral-free funding, minimal documentation, and quick approvals—making it a game-changer for small business owners.

If you’ve been struggling to secure funds for your business, this guide will walk you through everything you need to know—from eligibility to application—so you can take full advantage of this opportunity.

SME Asaan Finance (SAAF) Scheme.

What Makes the SAAF Scheme Different?

The SAAF Scheme isn’t just another loan—it’s a tailored financial solution for SMEs that removes traditional banking barriers. Here’s what sets it apart:

1. No Collateral, No Stress

- Unlike traditional loans that require property or assets as security, SAAF is 100% collateral-free.

- Perfect for startups and small businesses that don’t own high-value assets.

2. Simplified Application Process

- Minimal paperwork—no endless documentation loops.

- Faster approvals (often within 7-10 working days).

3. Flexible Loan Amounts & Tenures

- Borrow from PKR 100,000 up to PKR 10 million.

- Repayment periods ranging from 1 to 5 years, depending on business needs.

4. Competitive Profit Rates

- Lower markup rates compared to conventional SME loans.

- Islamic financing options available through Meezan Bank and other participating banks.

5. Supports Diverse Business Sectors

- Available for manufacturing, trading, and services.

- Ideal for retailers, wholesalers, small factories, and service providers.

Who Meets the Criteria?

The SAAF Scheme is designed to be inclusive, but there are a few key requirements:

✅ Business Requirements

- Must be a registered SME (sole proprietorship, partnership, or private limited company).

- Startups must have at least 6 months of operational history.

- Existing businesses should show consistent revenue (bank statements or sales records).

✅ Borrower’s Profile

- Registered Pakistani citizen with an active CNIC.

- No prior loan defaults with any financial institution.

❌ Who’s Not Eligible?

- Large corporations (businesses exceeding SME definitions).

- Individuals without a registered business.

- Applicants with a history of loan defaults.

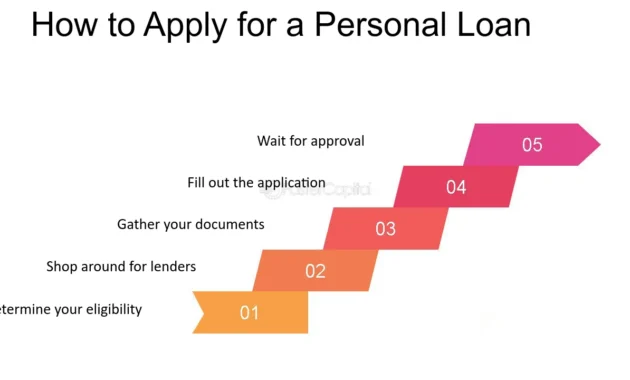

Step-by-Step Application Process

Getting a SAAF loan is straightforward if you follow these steps:

Step 1: Choose Where to Bank

Several leading banks in Pakistan offer the SAAF Scheme, including:

- HBL (Habib Bank Limited)

- UBL (United Bank Limited)

- MCB Bank

- Allied Bank

- BAFL (Bank Alfalah abbreviation)

- Meezan Bank (for Sharia-compliant financing)

💡 Pro Tip: Compare profit rates and terms across banks before applying.

Step 2: Complete Your Document Checklist

The SAAF Scheme requires minimal paperwork, but you’ll need:

- Business CNIC/NTN certificate (if registered).

- Applicant’s CNIC copy.

- Last 6 months’ business bank statements.

- Proof of business address (utility bill or rental agreement).

Step 3: Turn In Your Application

- Go to the closest branch of the bank you’ve selected.

- Some banks allow online applications (check their website).

Step 4: Loan Assessment & Approval

- The bank evaluates your business viability.

- If approved, funds are disbursed within days.

Why Should You Consider SAAF? (Key Benefits)

Still on the fence? Here’s why thousands of Pakistani SMEs are turning to SAAF:

🚀 Fast Access to Capital

- No long waiting periods—get funds within days, not months.

💡 No Need for Property or Guarantors

- Perfect for entrepreneurs who don’t own land or assets.

📈 Fuel Business Growth

- Use funds for:

- Expanding operations

- Purchasing inventory

- Upgrading machinery

- Hiring staff

⚖️ Flexible Repayment Options

- Choose a tenure that suits your cash flow (up to 5 years).

🤝 Government-Backed Security

- Backed by the State Bank of Pakistan, ensuring credibility.

Common Questions Answered (FAQs)

Can individuals working from home or running freelance operations apply?

Yes, if they’re registered as a business and meet the 6-month operational requirement.

What if I don’t have a business bank account?

You’ll need to open one—banks require 6 months of transaction history.

Is there any cost associated with the application process?

Some banks charge a small fee (usually 1-2% of the loan amount).

Can I apply if I already have a loan?

Yes, but your debt-to-income ratio must be within bank limits.

What happens if I default?

Defaulting will blacklist you from future loans—always repay on time!

Final Verdict: Is SAAF Right for You?

If you’re a small business owner struggling to secure funds, the SAAF Scheme is one of the best financial tools available in Pakistan today. With no collateral, quick processing, and flexible terms, it eliminates the biggest hurdles SMEs face.

Ready to take the next step? Visit your nearest participating bank or check their website to start your application today!

Byline: “Empowering Pakistan’s SMEs—one loan at a time.

")

")

")

{kind=link}